8-9 / 76

8-9 / 76

Industrial Market

Overview

Strong Demand Exceeds Supply

Occupier demand continues to grow

as the construction, manufacturing and

distribution sectors remain buoyant

given the strong economic climate and

business confidence. Occupiers are

continually searching for higher quality

and larger premises with supply unable

to keep up with the increased demand.

This has caused vacancy rates to fall

to record low levels across the board

with current vacancy levels in Mount

Wellington, Penrose and Onehunga

showing the biggest decline currently

below 2%, whilst vacancy within East

Tamaki has remained low currently

below 3%.

Developers who have land banked

essentially control new supply and

are seeing the benefit of their actions

from increasing land prices and an

increased buyer pool of investors

seeking out modern buildings with

strong tenant covenants. The lack

of industrial zoned land available

for development has caused prices

to increase to upwards of $400 per

square metre in the popular South

Auckland localities increasing to over

$500 per square metre for centralised

localities. The increasing cost of land

coupled with increased construction

and labour costs is causing pressure

on the margins for a number of

developers causing further pressure

on supply.

As the land in the popular suburbs

continues to be increasingly scarce,

there has been an increase in the

number of occupiers and developers

purchasing land further abroad from

the popular localities in order to meet

their size and cost requirements. An

example is the new industrial area

along Oruarangi Road, adjacent to

Auckland Airport which is becoming

increasingly popular with occupiers

given the large site sizes and close

proximity to Auckland Airport. Land

values in the area continue to rise;

Knight Frank has recently sold a 1.04

hectare site at 576 Oruarangi Road,

Mangere for $380 per square metre.

Comparing this with the price that

would have been achievable 18 months

ago in the vicinity of $250 - $300 per

square metre, it is evident land value

prices are growing at a rapid rate.

Knight Frank forecasts land value

growth will continue through 2016.

The Auckland industrial market has

been very positive heading into 2016

as the unprecedented demand from

both occupiers and investors has

caused constraints in the market.

Vacancy rates are continuing to decline to record lows as

new supply has struggled to keep up with demand with

development being slow for the past 24 months. As a result

the rental market has heated up with industrial rentals rising

sharply over the past 12 months as occupiers are struggling

to find space. The high occupier demand, low interest

rates, strong investor confidence and competition between

occupiers and investors has caused sale prices to rise and

yields to contract to record levels. The market is showing

little signs of slowing with 2016 looking to be a record year.

FIGURE 1

Percentage of properties per suburb

FIGURE 2

2016 vacancy % outlook

FIGURE 3

Auckland building consent values – factories, industrial & storage

Current Stock and Building

Consents

The following charts outline the

total number of properties and total

floor area per suburb. For the South

Auckland Industrial areas, East Tamaki

leads the way with 32% of the total

number of industrial properties and

caters for 27% of the total floor area.

Penrose

Mt Wellington

Onehunga

Manukau/Wiri

East Tamaki

Airport

Industrial Rents Surge

The strong occupier demand coupled

with the shortage in supply has

caused South Auckland Industrial

rents to surge across the board. Rental

levels of prime and secondary grade

properties have increased over the

past 12 months, with new design and

builds in the central localities leading

the way. Knight Frank is aware of prime

industrial buildings reaching levels

of upwards of $125 per square metre

for warehouse space and $230 per

square metre for offices. We anticipate

the trend likely to continue throughout

2016 whilst vacancy rates remain at an

all-time low. The secondary industrial

market is receiving the overflow

benefits from the lack of prime stock

available. With strong demand for

prime quality space, coupled with the

shortage of supply and the resultant

increase in rentals, some occupiers

are looking to secondary stock and

carrying out purpose built fitouts and

alterations. The result being that rental

levels and demand for secondary

stock has increased greatly over the

past 12 months with rental rates in

the main South Auckland Precincts

ranging from $85-$100 per square

metre over the warehouse.

Landlords are becoming more

Charles Vaughan

Registered Valuer

+64 9 377 3700

charles.vaughan@ nz.knightfrank.comTim Gemmell

Director – Valuation,

South Auckland

+64 9 377 3700

tim.gemmell@ nz.knightfrank.com15%

15%

32%

14%

16%

8%

July 2016 Vacancy %

Penrose/Onehunga

1.9%

East Tamaki

2.7%

Mount Wellington

1.2%

Manukau/Wiri

2.4%

Airport Corridor

1.9%

2012

2013

2014

2015

2016

$

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

$300,000,000

$350,000,000

$400,000,000

$450,000,000

East Tamaki is also the home to the

Goodman owned Highbrook Business

Park which commenced construction

in 2004 and has been very successful.

Set over 107 hectares, it delivers prime

commercial and industrial design and

build leaseback space options.

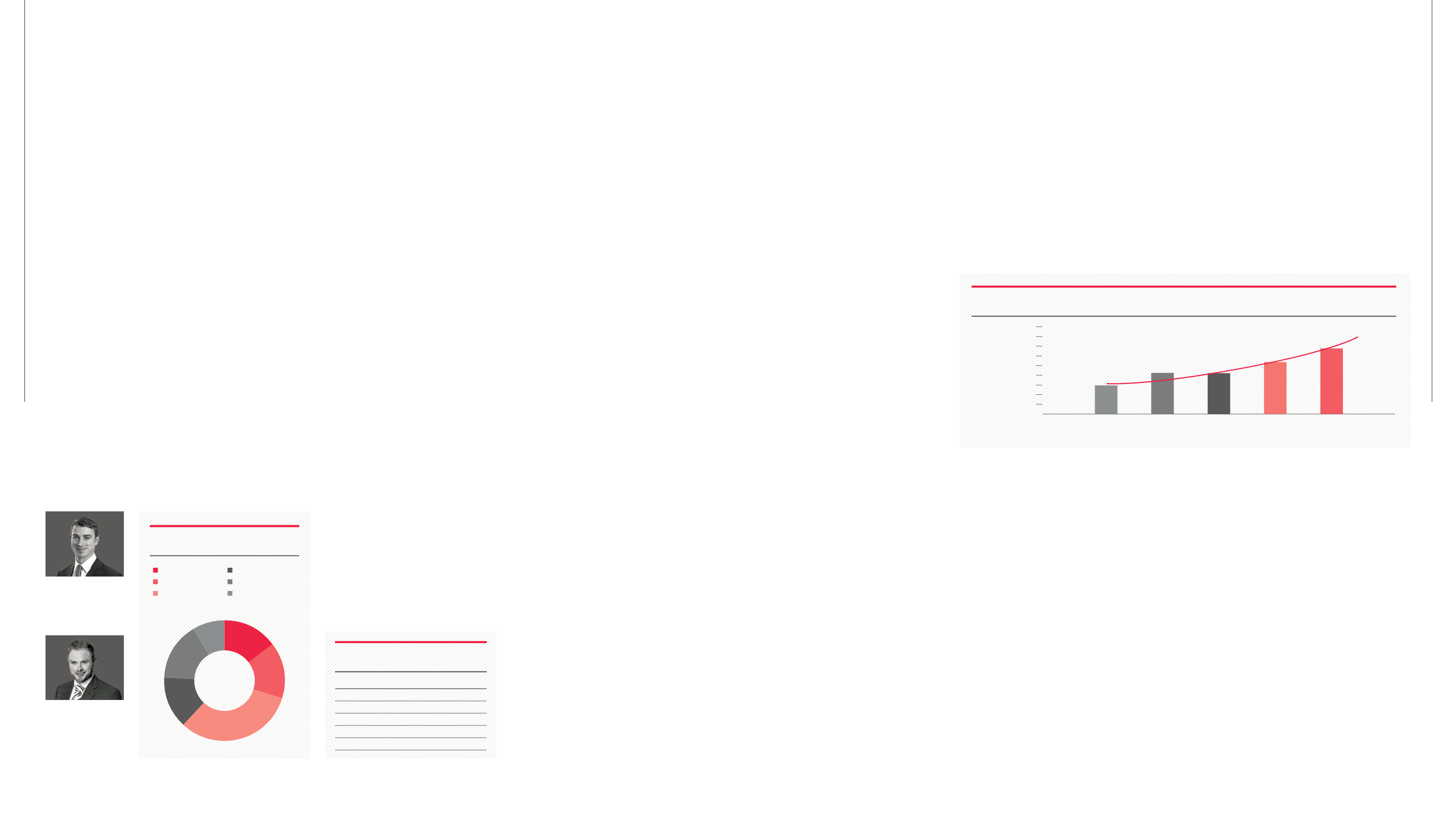

The upward trend for industrial

building consent values has continued

with Q3 2015 – Q2 2016 seeing 149

applications totalling nearly $340

million dollars. The building consents

from the last 12 months show that just

over 330,000 square metres of new

industrial stock will be introduced to

the market in the coming 12 months.

There has been a consistent trend of

increasing building consent numbers

over the past 24 months as the new

supply struggles to keep up with

demand. The increasing trend in

new supply is likely to continue over

the next 12 months as a number of

the heavyweight developers such

as Goodman, Southpark, James

Kirkpatrick Group Limited and AIAL

look to take advantage of the strong

occupier demand with new design

and builds. The indications are the

increased new supply will assist in

easing the current shortage as the

buildings become available in 2017.

aggressive in their approach to letting

up premises compared to 24-36

months ago. The low vacancy rates

have meant incentives have all but

disappeared from the market place

where they were typically present

after the GFC. The length of lease

terms have also increased with

occupiers being required to sign

up to longer lease terms in order to

secure premises given the increasing

competition. This coupled with the

lack of alternative premises to move

to at expiry has well and truly made

it a landlords market. The increase in

rentals here also meant tenants have

to stomach sizeable rental increases

as market review dates fall due.

Knight Frank has seen evidence of

rental levels increasing at a rate of

over 5% per annum in the past 12

months. We anticipate this trend to

continue throughout 2016; however

with the new supply coming online

in 2017 we expect the inflationary

pressure to slow.

AUCKLAND

AUCKLAND

8

PROPERTY VIEW 2016

KNIGHTFRANK.CO.NZ9